Recession glam beauty is reshaping Asia Pacific – a market worth $183 billion that grew just 1.4% in 2024, while Vietnam fragrance sales jumped 31% and value-tier brands captured double-digit share from established players. The divergence is not a contradiction. It is the clearest expression of what Euromonitor International has named the defining consumer trend across Asian markets: “recession glam,” a structural shift in how consumers define premium, where perceived value and purpose matter more than price tier.

What Recession Glam Actually Describes

The term is more precise than it sounds. Recession glam does not describe consumers buying cheap products. It describes consumers redefining what “worth it” means – and spending selectively on categories and formats that deliver tangible emotional or functional return at a manageable price point.

Euromonitor’s Yang Hu, Asia Pacific insight manager for health and beauty, frames it directly: “The definition of premium is changing – less about price, more about perceived value and purpose.” The behavioral indicators are specific: buying mini-size products, finding deals on trusted brands, reducing the number of steps in a routine, purchasing multifunctional products, and migrating from prestige to mass brands that can substantiate their claims.

The category that best illustrates recession glam mechanics is fragrance. A bottle of perfume at $30–$60 delivers a daily sensory experience, signals personal identity, and lasts months. Compared to a $120 serum that may or may not deliver visible results in six weeks, the fragrance is the better value proposition for a consumer under economic pressure. This is why fragrance outperformed skincare across Asia in 2024 – not because consumers love fragrance more, but because the value equation is more legible.

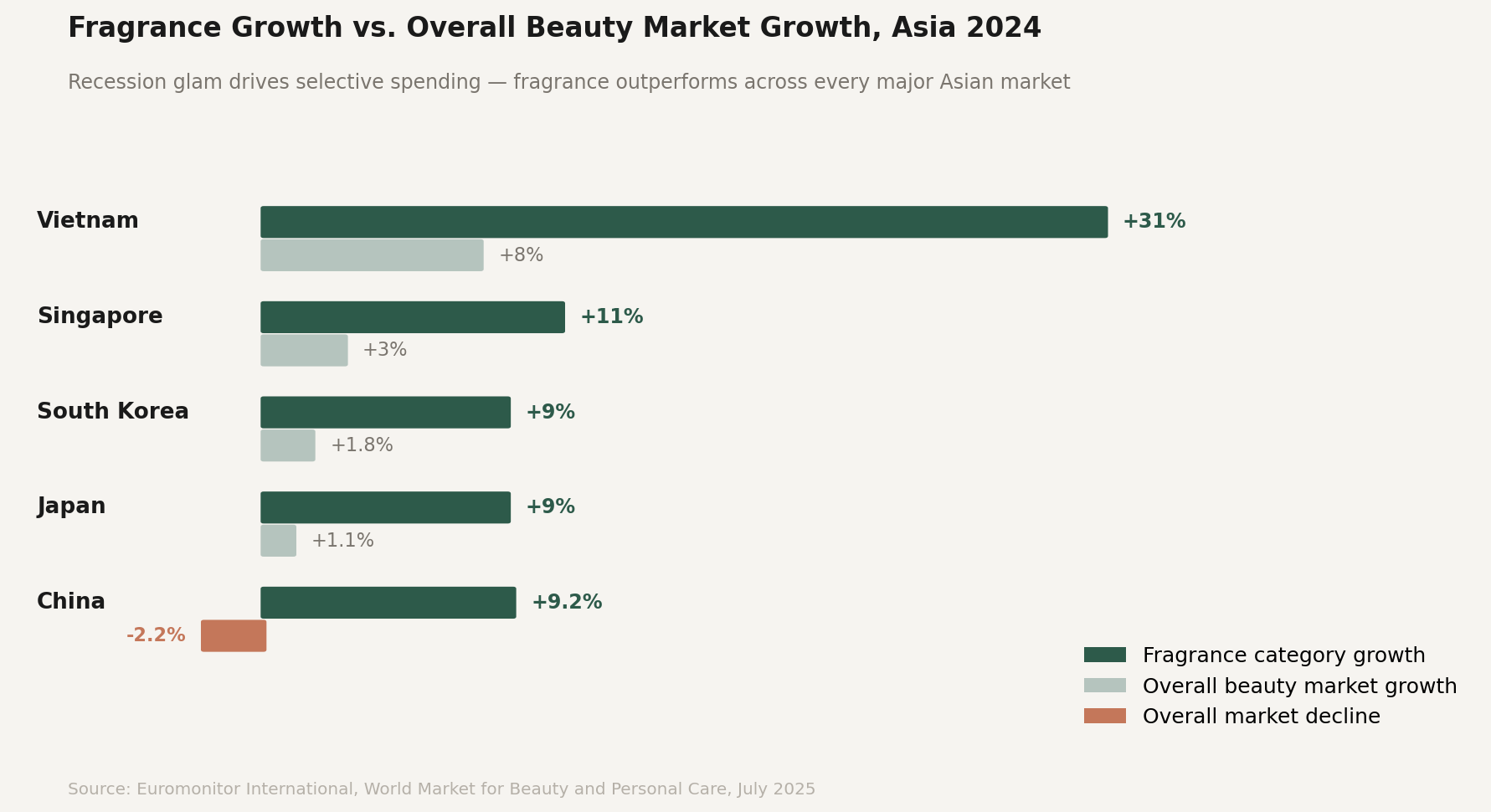

The Numbers Behind the Shift

Asia Pacific accounted for 31% of global beauty and personal care sales in 2024, representing $183 billion. Despite that scale, regional growth was just 1.4% – compared to SEA (excluding Singapore), which is projected to lead Asia at 5% annual growth over the next five years, according to Euromonitor.

The fragrance data is the most telling. South Korea and Japan each recorded 9% fragrance growth in 2024 against overall market growth of 1–2%. China saw a CAGR of 9.2% for premium fragrances even as its overall beauty market declined 2.2%. In Southeast Asia, Singapore recorded 11% mass fragrance growth – the highest in over a decade – and Vietnam recorded 31% fragrance growth driven by the entry of global fragrance brands into retail.

These numbers share a common logic: consumers are not stopping spending on beauty. They are concentrating spending on categories where the value proposition is clear, the format is accessible, and the emotional payoff is immediate.

The private label and value-tier dynamic reinforces the same pattern. Chinese brand Pinkflash captured meaningful share in SEA markets with color cosmetics priced between $1 and $6. In Indonesia, Chinese brands collectively grew from 2% to over 15% of the mass color cosmetics share between 2019 and early 2025. The growth is not driven by brand equity – it is driven by price-to-performance credibility at a spending level that SEA consumers can sustain.

What This Means for V-Beauty Specifically

Vietnamese beauty brands sit at an unusual intersection of the recession glam dynamic. They are not mass-market price competitors – Cocoon’s hero serums are priced at a mid-premium level that puts them above Chinese value-tier competitors. They are not prestige brands whose pricing depends on heritage and aspiration. Furthermore, they occupy a position that recession glam is actively creating demand for: brands with genuine ingredient provenance and substantiated claims at accessible premium price points.

The specific attributes that Vietnamese brands have built – ingredient-region storytelling, climate-adapted formulation, and cruelty-free certification – are precisely the “perceived value and purpose” attributes that Euromonitor identifies as the new definition of premium. A consumer trading down from a $120 La Mer moisturizer is not looking for the cheapest product available. They are seeking a product they can believe in at a price they can justify. Vietnamese skincare’s position – authentic botanical ingredients, traceable provenance, and formulations built for tropical conditions – is well-aligned with that decision framework.

The format gap is the more immediate opportunity. Recession glam is driving demand for trial sizes, mini formats, and entry-level SKUs that allow consumers to test efficacy before committing to full-size purchases. This is where Vietnamese brands are currently weakest in international distribution. Most Vietnamese skincare brands distribute primarily in full-size formats through e-commerce channels. The mini-size and trial-pack infrastructure that would allow international consumers to discover Vietnamese skincare at low financial risk – the discovery format that drove K-beauty adoption in Western markets – largely does not exist for V-beauty yet.

The Competitive Pressure Is Already Here

The same recession glam dynamic that creates opportunity for V-beauty also creates urgency. The affordable-luxury gap that Vietnamese brands could fill is already attracting competitors with more distribution infrastructure.

Chinese brands are moving into SEA with aggressive pricing and social commerce mechanics that V-beauty currently cannot match at scale. K-beauty’s dermocosmetics segment – brands like Aestura, Physiogel, and Medicube that deliver clinical positioning at accessible prices – is growing 13% annually in Korea and expanding internationally. These are not luxury brands. They are the exact value-premium hybrid that recession-glam consumers are seeking, and they have international distribution that most Vietnamese brands do not.

The window in which Vietnamese beauty brands can establish themselves as the credible, affordable premium option in SEA and international natural beauty channels is defined by how quickly those competing categories consolidate their recession glam positioning. It is not unlimited.

The V-Beauty Recession Glam Playbook

The brands most likely to benefit from recession glam in Vietnamese beauty share three characteristics that are visible in the market now.

Format expansion is the first. Brands that introduce trial sizes, travel formats, and starter kits at sub-$20 price points create the discovery infrastructure that drives long-term retention. Cocoon’s Amazon presence gives it the platform – the missing piece is the format strategy that converts first-time buyers into repeat customers.

Value articulation is the second. Recession glam consumers do not respond to “luxury” language – they respond to specificity. “Vitamin C serum” is less compelling than “22% ascorbyl glucoside brightening serum, Hung Yen turmeric origin.” The ingredient-region storytelling that Vietnamese brands have built for the domestic market is precisely the value articulation language that international recession-glam consumers are trained to respond to. The brands that translate that story into international retail vocabulary will have a competitive advantage.

Channel alignment is the third. Recession glam is driving consumers toward channels that combine discovery, value, and trusted curation – TikTok Shop, Amazon’s clean beauty sections, specialist Asian beauty retailers. These are not channels that require the same distribution investment as physical retail entry. They are channels where Vietnamese brands can compete now, at the current scale, if the product and story are right.

The macroeconomic conditions that created recession glam are not temporary. Inflation, constrained disposable income, and increased consumer skepticism of premium price premiums are structural features of the post-pandemic consumer landscape across Asia and beyond. Vietnamese beauty brands that understand recession glam as a positioning opportunity rather than a threat have a longer runway than the current coverage gap suggests.

Sources: Euromonitor International, World Market for Beauty and Personal Care, July 2025 (via WWD, Premium Beauty News, Euromonitor.com press release); Jing Daily, Euromonitor: Asia Pacific beauty shoppers buy less, use less, August 2025; Future Market Insights, SEA C-Beauty Product Market Forecast to 2035; Dewsia, Cocoon Vietnam: Everything You Need to Know.