In February 2026, Marico announced the acquisition of a 75% stake in Skinetiq – the Vietnamese D2C company behind skincare brand Candid – at a valuation of approximately $40 million, its second Vietnamese beauty deal in three years. The acquisition is worth examining not for what it tells us about Marico’s ambitions, which are now clear, but for what it tells us about what happens to local Vietnamese beauty brands once a conglomerate arrives. What that means for the brands that haven’t been acquired yet.

What Marico Is Actually Buying

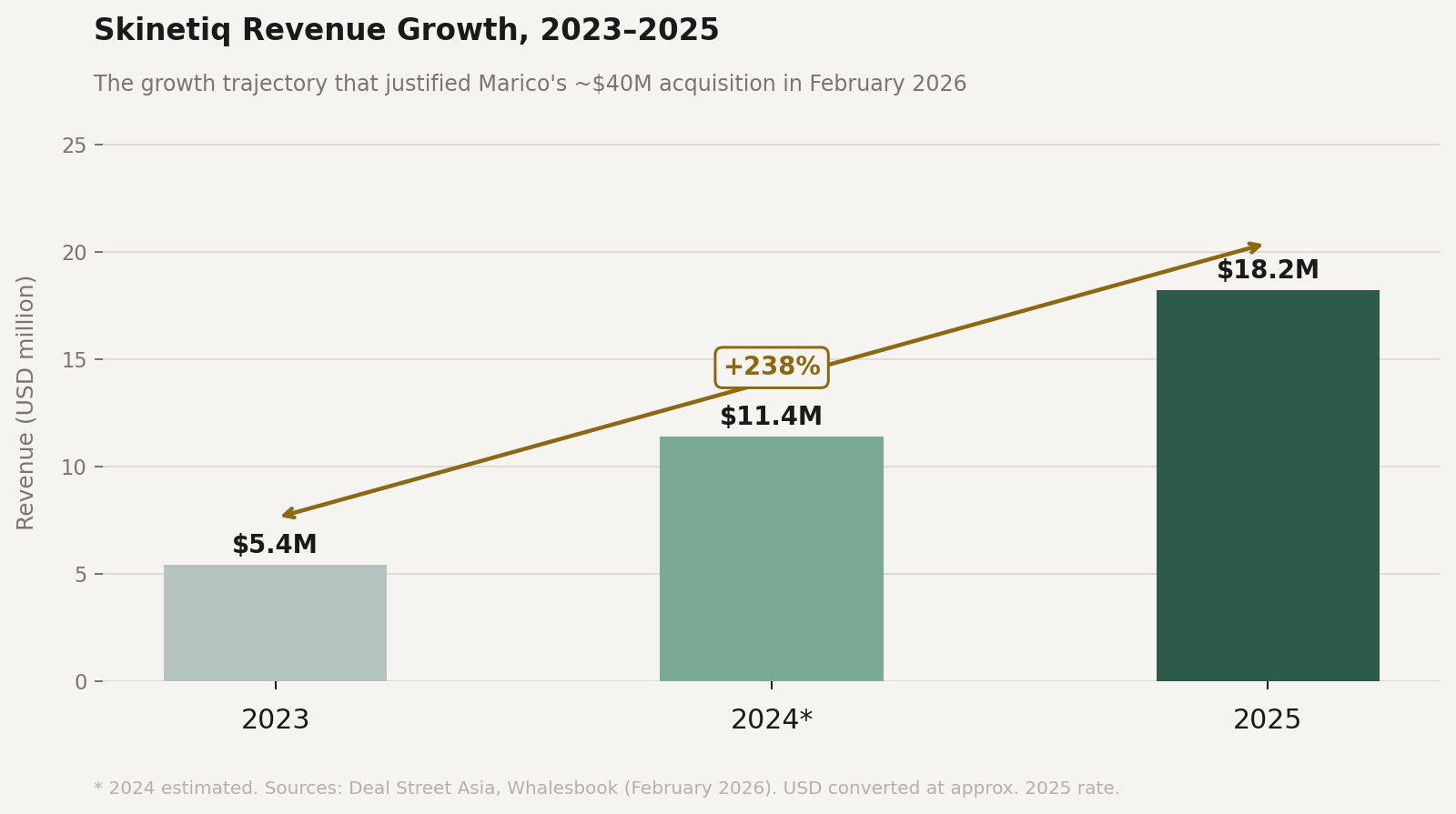

Skinetiq is not a heritage brand. Founded in 2020, it is a digital-first company that built Candid – a science-backed skincare line targeting the mid-premium segment – almost entirely through social commerce, dermatology-led content, and a community of digitally savvy young consumers. Revenue grew from approximately $5.4M in 2023 to $18.2M in 2025, with EBITDA margins in the mid-twenties. Marico paid roughly 2.3x projected 2025 revenue – a premium valuation by any measure.

The strategic logic from Marico’s perspective is straightforward. Skinetiq has built what large consumer goods companies consistently fail to build organically in digital-native markets: a credible brand with genuine consumer relationships, growing profitably in a channel – social commerce and D2C e-commerce – that Marico’s legacy distribution infrastructure cannot access efficiently. The acquisition buys the brand equity, the channel expertise, and the consumer data. Marico’s scale provides the manufacturing efficiency, supply chain optimization, and capital for expansion.

Marico CEO Saugata Gupta framed the deal explicitly: “Skinetiq’s digital-led model and science-backed portfolio align seamlessly with Marico’s vision for the future of beauty and portfolio premiumization.” The language is precise. Marico is not buying a heritage ingredient story. It is buying a distribution model.

The Template and Its Precedents

Marico’s approach to acquired brands in India provides the most direct evidence of what happens post-acquisition – because the pattern is visible across multiple cases over nearly a decade.

Beardo, the men’s grooming brand Marico acquired a 45% stake in during 2017 before buying full control in 2020, is the most instructive example. In the years immediately following acquisition, Beardo maintained its brand identity and grew rapidly – Marico cited it as a growth contributor in multiple earnings calls. The challenge came in the medium term: distribution expansion into modern trade and e-commerce channels brought Beardo into direct competition with Marico’s own portfolio of male grooming products. Brand positioning gradually shifted from premium D2C toward accessible mass-market, a movement driven by margin pressure and the logic of scale.

True Elements, a health food brand Marico acquired a majority stake in during 2022, followed a similar trajectory. The brand’s premium positioning and loyal direct consumer base were the stated rationale for acquisition. Post-integration, distribution expanded, pricing was repositioned, and the brand’s identity – while not destroyed – became progressively harder to distinguish from the broader Marico wellness portfolio.

The pattern is not unique to Marico. Unilever’s acquisition of smaller Southeast Asian personal care brands consistently produces the same outcome: initial growth under acquired management, followed by integration pressure, followed by either brand dilution or quiet discontinuation. The economics are structural, not intentional. A conglomerate with Marico’s scale cannot justify maintaining the operational overhead of a premium D2C brand unless that brand either grows into meaningful revenue contribution or gets absorbed into existing channels. Growth requires scale. Scale requires distribution. Distribution commoditizes.

What This Means for Skinetiq Specifically

Skinetiq’s positioning – clinically credible, mid-premium, digital-first – is precisely the kind of brand that survives post-acquisition best, because its value proposition is tied to a specific channel and consumer relationship rather than purely to ingredient heritage or cultural narrative.

The risk is not that Marico will deliberately undermine Candid. The risk is that the operational logic of integration gradually modifies the brand’s decisions in ways that, individually, seem rational but cumulatively reshape its identity.

Pricing discipline is the first pressure point. Marico’s scale creates cost-reduction opportunities – better raw material sourcing, more efficient manufacturing, shared overheads. Each cost reduction creates space for either margin improvement or price reduction. For a brand competing on clinical efficacy at mid-premium pricing, modest price reductions initially expand the addressable market. Over time, they reposition the brand relative to the clinical skincare competitors – La Roche-Posay, Eucerin, the Korean derma brands – that defined the segment in which Candid was competing.

Channel expansion is the second. Skinetiq built its business through social commerce and D2C. Marico’s existing Vietnam operations include Guardian stores, Watsons, and modern trade channels. Expansion into those channels is the obvious next step. But shelf placement in physical retail requires different packaging economics, different promotional mechanics, and different product formats than D2C social commerce. Each accommodation to retail channel requirements is a small departure from the brand’s founding logic.

The question is not whether these pressures will exist. They will. The question is whether Skinetiq’s founders, who retain 25% and have milestone-based earn-out incentives, have sufficient influence through 2028 to maintain the brand’s positioning during the critical integration period.

The Cocoon Question

Cocoon – Vietnam’s most internationally visible beauty brand, the best-selling brand at Guardian Vietnam in 2025, certified by PETA and Leaping Bunny, with distribution reaching the US, Canada, Australia, and Malaysia – has not been acquired. It remains owned by Nature Story Cosmetics Company Limited, its founding company.

It is also, by most measures, the obvious next acquisition target in Vietnamese beauty.

The brand has everything a consumer goods conglomerate would want: genuine international visibility, a defensible brand narrative built on Vietnamese ingredient provenance, cruelty-free certification that opens premium international retail, and demonstrated domestic consumer loyalty. Its vegan positioning is structurally differentiated in a category – natural beauty – that is growing at approximately 2.5% annually within Vietnam’s broader market.

The acquisition logic would differ from Skinetiq. Skinetiq was a distribution model acquisition. Cocoon would be a brand equity acquisition – buying the story, the certification, and the international potential. Marico already has Vietnamese distribution through MSEA. What it does not have is a brand with Cocoon’s international narrative credibility.

The more interesting question is not whether Cocoon will eventually attract acquisition interest. It is whether Cocoon can reach the international distribution scale that would make its acquisition value compelling before acquisition pressure makes remaining independent difficult. The brand is available in 130 Guardian stores in Vietnam and on Amazon internationally. The gap between that distribution and the shelf presence of K-beauty competitors in equivalent international markets is significant.

What Both Cases Reveal About V-Beauty’s Trajectory

The Skinetiq deal and the Cocoon question illuminate the same structural dynamic from different angles.

For Skinetiq, the acquisition provides capital and scale that the brand could not access independently. The risk is that conglomerate ownership gradually modifies the brand’s identity. For Cocoon, independence preserves brand integrity but limits the distribution investment required to close the gap with international competitors.

Neither path is obviously superior. What both paths share is a dependence on decisions made in the next two to three years – before Marico’s integration of Skinetiq is complete, and before Cocoon’s international distribution either reaches meaningful scale or stalls. Before the next wave of conglomerate attention arrives in Vietnam’s beauty market.

Marico has now made three meaningful commitments to Vietnamese beauty in three years. L’Oréal is naming Vietnam in its annual results as a key growth contributor. Alibaba acquired a minority stake in Hasaki, Vietnam’s largest beauty retail chain, in 2023. The pattern of external capital arriving in Vietnamese beauty is accelerating, not decelerating.

For locally founded Vietnamese brands, the window to establish international distribution infrastructure on their terms is narrowing. Acquisition provides scale but reshapes identity. Independence preserves identity but limits scale. The brands that navigate this tension successfully will be the ones that define what V-beauty means internationally – and the choices being made now will determine which brands those are.

Sources: Deal Street Asia, Marico acquires 75% stake in Vietnam’s Skinetiq JSC (February 2026); Vietnam News, Marico expands Vietnam presence with majority stake in Skinetiq (February 2026); Business Upturn, Marico completes acquisition of 75% stake in Vietnam’s Skinetiq (April 2026); Vietnam.vn, Cocoon cosmetics was the best-selling brand at Guardian Vietnam in 2025 (January 2026); Business Standard, Marico to acquire Vietnamese personal care brands Purité de Provence, Ôliv (December 2022); Dewsia, Cocoon Dak Lak Coffee Scrub Review; Dewsia, Where to Buy Vietnamese Skincare Products.