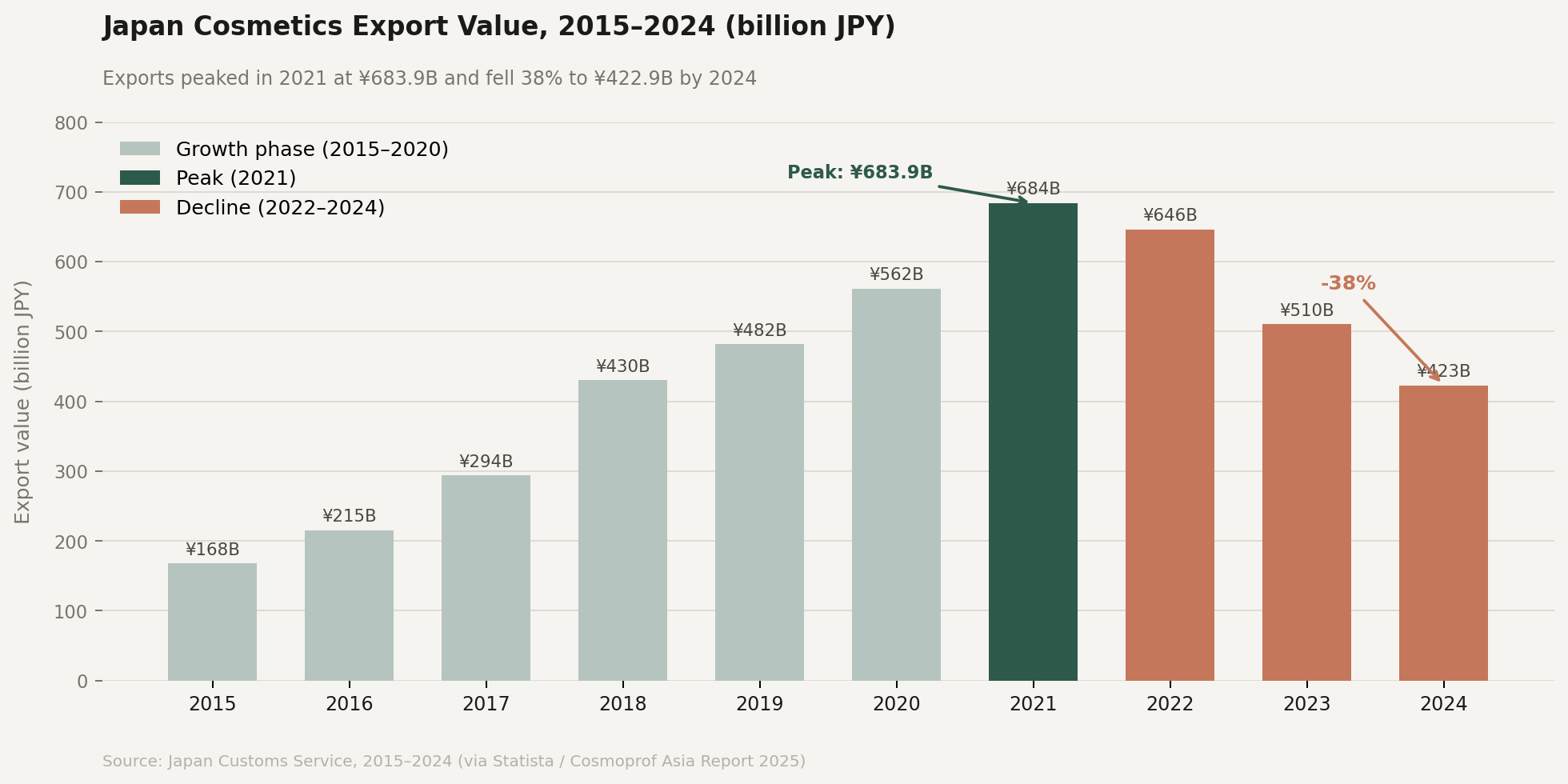

Japan beauty exports peaked at 683.9 billion yen in 2021 and fell to 422.9 billion yen by 2024 – a 38% decline in three years, while South Korea hit a record $11.4 billion and France grew 6.3% over the same period. The collapse is real and documented. What it means, however, depends on which Japanese company you are looking at – and the divergence between them is as instructive as the aggregate number.

The China Dependency That Built J-Beauty’s Export Decade

Japan’s export growth between 2015 and 2021 was built almost entirely on one market. China has accounted for the majority of Japanese cosmetics export value since 2020, according to Japan Cosmetic Industry Association data. The rapid expansion of Chinese middle-class consumption, the strong preference for Japanese brands among premium beauty buyers, and the boom in daigou trading and travel retail all created conditions that allowed Japanese brands to grow exports at double-digit rates. Without building meaningful distribution in any other major international market.

That model had a structural fragility built into it from the beginning. Export revenue concentrated in a single market is not international expansion – it is dependency. When China’s consumer sentiment shifted, when domestic brands gained credibility, and when the daigou and travel retail channels collapsed post-pandemic, Japanese brands had no diversified export base to absorb the shock.

The consequences are visible in every Japanese conglomerate’s results. Shiseido’s China and travel retail business fell 3.5% for the full year 2025, with the first half bearing double-digit declines before a partial recovery. The company’s net sales declined 2.1% year-on-year despite a 22% rise in core operating profit – a gap explained entirely by aggressive cost reduction rather than revenue growth. Pola Orbis dissolved its Orbis Beijing subsidiary in 2025 after three consecutive years of losses, recording an extraordinary loss of approximately 1.3 billion yen. Kosé reduced staff in its Chinese operations and merged its China sales subsidiary as part of a broader restructuring.

The Numbers Behind the Decline Are Sectorwide – Not Company-Specific

The export data from Japan Customs confirms that the decline is not a Shiseido story. It is a J-beauty story.

Japan’s total cosmetics export value fell from its 2021 peak of 683.9 billion yen through 510.5 billion yen in 2023 to 422.9 billion yen in 2024. The trajectory is consistent and multi-year. It predates specific corporate decisions and reflects a market-level realignment rather than individual brand failures.

The concentration of Japanese beauty exports in Northeast Asia – China, Hong Kong, South Korea, and Taiwan – means that any deterioration in Chinese demand has an outsized effect on the aggregate export figure. Vietnam and Thailand do not appear as named destinations in publicly available Japan Customs country-level breakdowns, which itself reflects the limited operational infrastructure that Japanese brands have historically built in Southeast Asia.

What made this dependency particularly damaging is the nature of the channel through which it operated. Travel retail and daigou – informal reseller networks – are not stable distribution infrastructure. They generate revenue efficiently in good conditions but provide no brand equity, no direct consumer relationships, and no resilience when conditions change. Japanese brands that grew their China exposure through these channels discovered in 2022 and 2023 that their market position was shallower than their revenue figures suggested.

The Responses Are Not Uniform

The aggregate decline obscures meaningful strategic divergence between the major Japanese conglomerates – and that divergence is relevant for what comes next.

Shiseido has chosen the path of radical simplification. The company has reduced its brand portfolio to eight core brands, cut its global workforce by approximately 25% over five years, and concentrated investment on prestige positioning in Japan and selective international markets. Its 2025 results show the profit benefits of that strategy: core operating profit up 22%, and operating margins improving. The revenue line has not recovered, but the cost structure has been rebuilt.

Kao has taken a different approach. Its cosmetics division grew 7.2% in 2025, with sales reaching 261.6 billion yen. The growth came from two sources: strong performance of six focus brands in Japan and recovery in China supported by expanded local production and distribution optimization. Kao’s response to China’s weakness was not retreat – it was localization. The company invested in Chinese manufacturing capacity and rebuilt its channel economics from the ground up. Asia, and particularly China, showed “substantial” sales increases in 2025 as a direct result of that investment.

Pola Orbis has made the most explicit pivot toward Southeast Asia. Following the dissolution of its Beijing Orbis subsidiary, the company’s president named ASEAN as its designated growth driver for overseas business. The company has stated plans to double its SEA retail footprint by 2027, citing high-single-digit market growth expectations and rising incomes across the region. This is the first instance of a major Japanese beauty conglomerate publicly designating Southeast Asia – rather than China or the United States – as its primary overseas expansion target.

What the SEA Pivot Means in Practice

Pola’s SEA ambition is real, but the infrastructure gap it faces should not be underestimated.

Japanese beauty brands have historically operated in Southeast Asia through selective distribution: department store concessions, premium pharmacy counters, and imported products sold through specialist retailers. This model generates prestige positioning but limited scale. It also requires significant ongoing investment in retail staff training, product localization, and marketing that most Japanese brands have not historically committed to outside their core markets.

Building from a selective distribution base to a genuine mass-market or even mid-premium presence in markets like Vietnam, Thailand, or Indonesia requires years of investment in local partnerships, regulatory compliance, and consumer education. Kosé’s acquisition of Thai premium brand Pañpuri in 2024 is one model for this – acquiring local brand credibility rather than attempting to transplant Japanese brand positioning into unfamiliar markets. But it is a single data point, not a pattern.

The more immediate challenge is that Southeast Asian consumers, particularly in Vietnam and Thailand, already have deeply established preferences for Korean skincare. Vietnam’s K-beauty popularity stands at 70% – the highest of any country surveyed globally. Japanese brands arriving in this market are not entering a blank slate. They are competing against a Korean beauty infrastructure that has been building consumer relationships, distribution partnerships, and brand equity in the region for the better part of a decade.

The Structural Implication for Asian Beauty

Japan’s export decline is not a crisis in the conventional sense. The domestic market remains the world’s third-largest beauty market by revenue, and Japanese brands continue to command genuine prestige positioning globally. The decline is specifically a story about what happens when international expansion is built on a single market through unstable channels – and what the correction looks like when that market shifts.

The more significant question is not whether J-beauty recovers its 2021 export peak. It probably will not, at least not on the same geographic basis. The question is whether the strategic reorientation now underway – Shiseido’s brand consolidation, Kao’s China localization, Pola’s SEA pivot – produces a more durable international position than the travel retail-dependent model it is replacing.

For Southeast Asian markets, including Vietnam, the implication is direct. The J-beauty brands that arrive with genuine SEA investment – rather than selective distribution maintained as an afterthought to China strategy – will be competing for the same premium consumer that Korean brands are already cultivating. Domestic brands are beginning to target. The timing of that competition and the resources committed to it will determine whether J-beauty’s SEA chapter is a footnote or a genuine strategic shift.

Pola’s stated target of doubling its SEA footprint by 2027 is the clearest signal yet that at least one major Japanese conglomerate has decided the answer is the latter.

Sources: Japan Customs Service, cosmetics export data 2015–2024 via Statista/Cosmoprof Asia Report 2025; Shiseido FY2025 results via Cosmetics Business (February 2026); Kao Corporation FY2025 annual results via Cosmetics Business and Next In Beauty Mag (February 2026); Pola Orbis Holdings FY2025 financial summary via MarketScreener (February 2026); Pola Orbis SEA expansion announcement via CosmeticsDesign-Asia (March 2025); Japan Cosmetic Industry Association, import/export statistics; Korean Foundation for International Cultural Exchange, K-beauty Popularity Survey 2024.