V-beauty’s competitive window is narrowing. In 2025, more than 20 international beauty brands closed stores or withdrew from China. The exits cut across ownership structures, price tiers, and brand heritage – Laneige, SEKKISEI, Aesop, and TATCHA. These are not coordinated decisions. They are independent business judgments that have converged on the same conclusion: the Chinese premium market is maturing faster than it is growing. What has received less attention is where that capital is already going.

The Infrastructure Advantage Is Not Being Built. It Already Exists

The common framing of global beauty entering Southeast Asia treats the region as an emerging opportunity that large players are beginning to evaluate. For L’Oréal in Vietnam, that framing is outdated by several years.

L’Oréal’s Consumer Products division – which houses L’Oréal Paris, Garnier, Maybelline, and NYX – listed Vietnam alongside Brazil and Mexico as markets where “momentum was strong” in emerging markets. These are not comparable countries by population or economic size. What they share is a consumer products market growing faster than the global average, with distribution infrastructure that L’Oréal has spent years building. Vietnam’s inclusion in that list signals operational depth, not market entry.

The division’s brand-level reporting adds further context. 3CE, L’Oréal’s Korean color cosmetics brand, is cited as expanding throughout Southeast Asia – a region where L’Oréal is using an Asian brand identity to drive growth among consumers who are already deeply familiar with Korean beauty standards. The Dermatological Beauty division, L’Oréal’s fastest-growing globally at +5.5% like-for-like, identifies SAPMENA-SSA as its most dynamic region, led by La Roche-Posay and CeraVe.

The picture that emerges is not of a company positioning itself for future Vietnamese growth. It is of a company already generating that growth across multiple categories and price points.

L’Oréal does not need to build distribution in Vietnam. It already has it. The question for V-beauty is what that means for the competitive window that Vietnamese brands are currently operating within.

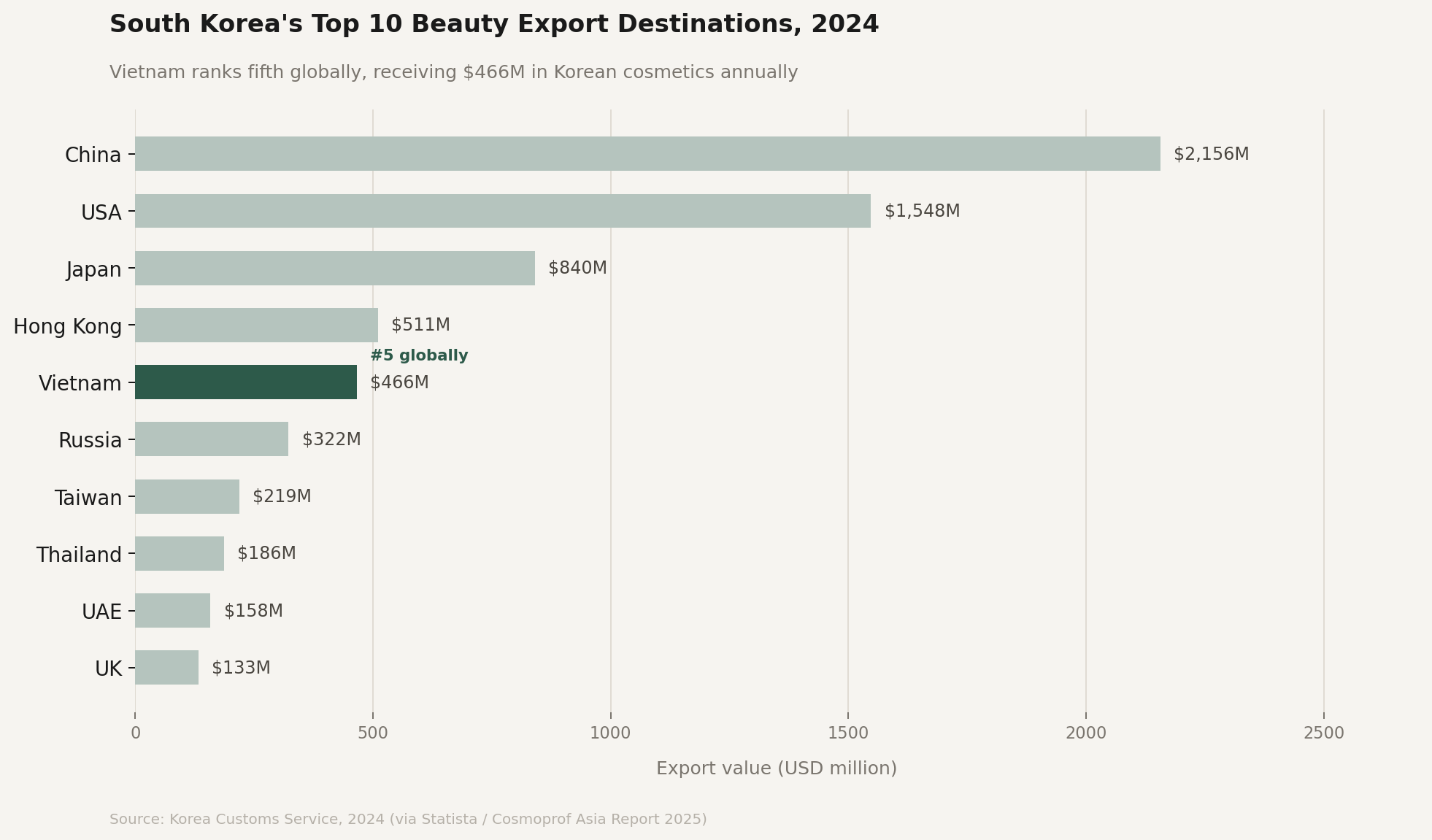

Vietnam Is K-Beauty’s Most Loyal Market – and That Is a Complication

Vietnam is K-beauty’s fifth-largest export destination globally, receiving $466 million in South Korean cosmetics annually, according to Korea Customs Service data. It is also the country with the highest perceived K-beauty popularity in the world: 70% of Vietnamese respondents in a 2024 survey by the Korean Foundation for International Cultural Exchange indicated that K-beauty was widely popular in their country. No other market in the survey came close.

These two data points create a specific problem for Vietnamese beauty brands. The consumer they are selling to – or hoping to sell to internationally – has been shaped by years of exposure to Korean skincare standards. The reference points for product texture, packaging quality, brand storytelling, and skincare routine logic have been set by an industry that invests billions annually in product development and marketing. The bar is not low, and it was not set by Vietnamese brands.

This does not mean V-beauty cannot compete. It means the competition is not being evaluated in a vacuum. When an international consumer encounters a Vietnamese skincare brand, the implicit comparison is not to nothing – it is to Laneige, COSRX, and Innisfree. That comparison is both an opportunity and a constraint.

The opportunity is differentiation: Vietnamese brands can offer something Korean brands genuinely cannot, which is authenticity around Vietnamese ingredient traditions, botanical heritage, and a skincare philosophy rooted in a different cultural and climatic context. The constraint is that differentiation requires a consumer who is already curious enough to seek it out – and that consumer is a smaller segment of the international market than the one K-beauty has spent a decade cultivating.

K-Beauty’s Pivot Has Left a Gap – But It Is Not the Gap V-Beauty Assumes

The narrative that K-beauty’s difficulties in China would redirect expansion capital toward Southeast Asia has not materialized in any systematic way. Amorepacific – the group behind Laneige, Sulwhasoo, and COSRX – reported its strongest operating profit since 2019 in 2025, with overseas revenue growing 15% and operating profit more than doubling. That growth is concentrated in Western markets. America’s sales more than doubled year-on-year in Q1. Southeast Asia appears in Amorepacific’s results under “other Asian markets” with no country-level breakdown and no disclosed targets.

The capital that left China did not flow to Vietnam. It flowed to Sephora.

What this does create, however, is a different kind of gap. K-beauty’s pivot toward Western prestige positioning – away from the accessible, trend-driven, digitally native model that made it dominant in Southeast Asia – opens space for brands that can serve the Vietnamese consumer on their terms. The consumer who bought Laneige through Shopee for the past five years is not necessarily loyal to K-beauty as a category. They are loyal to products that work, are accessibly priced, and carry a story they find compelling.

V-beauty can compete for that consumer. The question is whether it can do so at scale, with consistency, before L’Oréal’s existing infrastructure and brand portfolio fill the same space.

The Constraints and Structural Advantages Are Real

V-beauty’s case for international relevance is not manufactured. The ingredient depth is genuine – centella asiatica with a documented history of Vietnamese use, turmeric with centuries of functional application, and rice water with cultural provenance that no Korean or Japanese brand can claim for Vietnam. The price positioning is structurally competitive. The cultural proximity to the consumer base that will drive Asian beauty growth over the next decade is an asset that cannot be replicated.

The growth of Cocoon demonstrates that the category can produce brands capable of attracting serious capital. Marico’s acquisition was not speculative – it was a bet on distribution potential in markets where Marico already operates. The counterfeit networks operating across Shopee and Lazada for popular Vietnamese skincare products are, paradoxically, evidence of demand strong enough to fake. You do not build a sophisticated counterfeit operation around a product nobody wants.

The constraints are equally real and more immediate.

Distribution infrastructure outside Vietnam remains limited. The channels through which international consumers discover and purchase V-beauty products – specialist retailers, pharmacy chains, premium e-commerce – are either underdeveloped or dependent on third-party importers with limited incentive to build brand equity systematically. This is not a criticism of individual brands. It is a structural feature of an industry that is still primarily domestically oriented.

Clinical credibility is a related gap. The shift in premium beauty globally – documented most clearly in China but visible across markets – is toward efficacy-first purchasing. Consumers, and increasingly the retail buyers who decide which brands get shelf space, want clinical substantiation for ingredient claims. Vietnamese skincare brands with deep traditional ingredient heritage are, in most cases, not yet able to provide the kind of clinical evidence that would allow them to command premium positioning in regulated Western markets. That is not an insurmountable problem. It is a years-long investment.

Regulatory readiness for EU and US markets is a third constraint. “Clean” and “natural” claims that are standard in Vietnamese domestic marketing do not translate directly to markets where those terms carry legal definitions and certification requirements. A brand that positions itself on natural Vietnamese ingredients and then cannot substantiate those claims for import compliance is not ready for the markets where premium pricing is achievable.

The Window Is Defined by What L’Oréal Does Next

The competitive window for V-beauty is real. It exists because L’Oréal, despite its existing Vietnamese market position, is primarily growing there through mass-market consumer products and dermatological brands – not through a Vietnamese cultural narrative. That narrative space is unoccupied by any global player, and it is the space where V-beauty has a genuine and defensible advantage.

The window closes – or narrows significantly – when one of two things happens. Either a global player decides to invest in building that narrative authentically, which requires local brand acquisition or deep partnership rather than imported product. Or V-beauty brands fail to build the distribution and clinical infrastructure required to operate at an international scale before the mass-market positioning of global players becomes the dominant frame for how international consumers understand Vietnamese beauty.

Neither of those things is imminent. But neither is distant.

The brands that will define V-beauty’s international trajectory are the ones being built right now – with or without awareness of what L’Oréal’s 2025 results are signaling. The ones that read those signals clearly are in a better position than the ones that do not.

The window is not closing immediately. But the fact that L’Oréal is already in Vietnam, already growing, and already named it in its annual results is not a reason for optimism. It is a reason for urgency.

Sources: L’Oréal 2025 Annual Results (official press release, February 2026); Statista/Cosmoprof Asia 2025 Report (Korea Customs Service data); Korean Foundation for International Cultural Exchange, K-beauty Popularity Survey 2024; Amorepacific Group 2025 Earnings Summary (apgroup.com, February 2026); Korea Ministry of Food and Drug Safety cosmetics export data 2024.