Brightening skincare is the most commercially significant category in Southeast Asia – and it is fracturing. What was once a single segment defined by the aspiration for lighter, more even skin tone is dividing into two distinct product logics with different consumers, different price points, and different evidence requirements. Vietnamese beauty brands are naturally positioned for the premium half of that split. The problem is that natural positioning and market readiness are not the same thing.

How Brightening Became Two Markets

For most of the past decade, brightening operated as a unified category in Asian beauty. Products ranged from mass-market tinted moisturizers and tone-up creams to luxury serums, but they shared a common consumer promise: skin that looks lighter, more luminous, and more even in tone.

That unity is breaking down. Analysis of global e-commerce data from Q1 2025 shows that consumer demand around brightening has become “increasingly segmented, diversified, and functionally targeted.” The shift is visible in the terminology itself: where “brightening” was once sufficient as an efficacy claim, consumers – particularly in Korea and Japan but increasingly across Southeast Asia – are now searching for targeted language: anti-pigmentation, melanin inhibition, post-inflammatory hyperpigmentation, uneven skin tone correction.

This is not semantic drift. It reflects a fundamental change in what consumers expect brightening products to do and how they expect that performance to be substantiated.

The mass-market segment has responded with accessible tone-up products – tinted, SPF-enhanced formulas that deliver immediate optical brightening through physical mechanisms. These products are affordable, widely distributed, and require no clinical substantiation because their effects are visible and immediate.

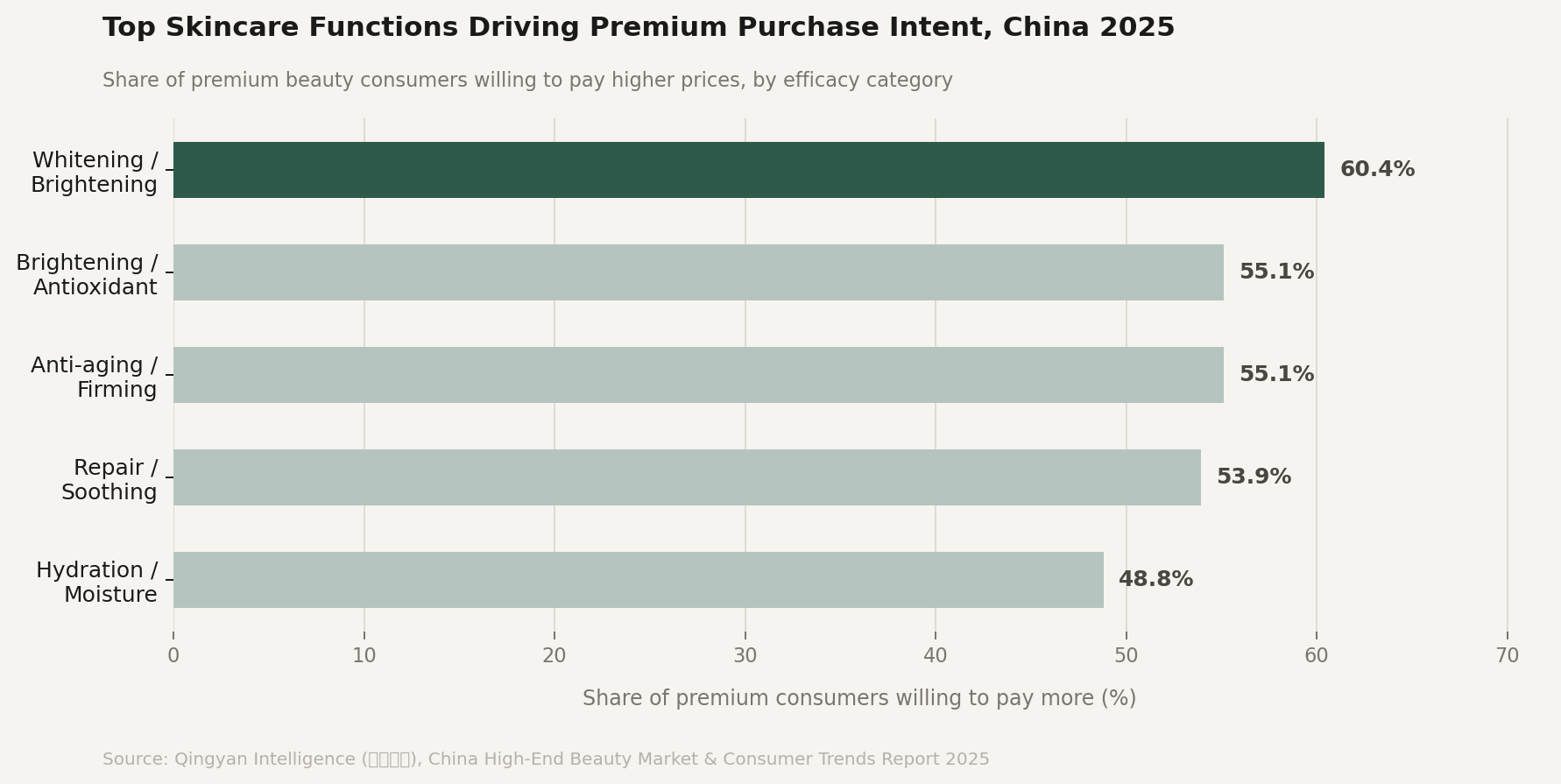

The premium segment is moving in the opposite direction. According to Qingyan Intelligence’s 2025 consumer data, whitening and brightening rank among the top two functional categories where premium Chinese beauty consumers express willingness to pay higher prices, with 60.4% of premium intent concentrated in these areas. But the same consumer data that shows high willingness to pay also shows that 79.1% of premium buyers cite efficacy and visible results as their primary purchase driver. This means premium brightening products must now demonstrate what they claim, not merely assert it.

What the Premium Brightening Consumer Now Requires

The functional brightening segment that is capturing premium consumer spending shares a set of characteristics that distinguish it clearly from tone-up products.

Clinical substantiation is increasingly non-negotiable. Products in this segment cite specific mechanisms: inhibition of tyrosinase enzymes, reduction of melanin transfer to keratinocytes, or suppression of post-inflammatory hyperpigmentation. L’Oréal’s Melasyl technology – the breakthrough anti-pigmentation ingredient behind La Roche-Posay’s fastest-growing product lines – is the clearest example of this model. The ingredient has clinical trial data, a named mechanism, and patent protection. It can be explained to a consumer, validated by a dermatologist, and compared against alternatives with measurable outcomes.

K-beauty has followed the same logic. Beauty of Joseon’s rice-based brightening line uses a combination of traditional ingredient storytelling and modern formulation science – niacinamide concentrations, rice bran fermentation processes. This allows the brand to speak simultaneously to consumers who respond to cultural heritage and consumers who respond to ingredient percentages. MIDHA’s patented “Rice 8 Complex” technology is a further step in the same direction: traditional ingredient, proprietary formulation, clinical language. Korean brands have learned, from watching the Chinese market shift, that heritage alone is insufficient when consumers begin comparing products on efficacy rather than on brand identity.

Dermatological distribution is becoming a marker of credibility in the premium brightening segment. Products sold through pharmacies, dermatology clinics, and medical aesthetics channels carry an implicit endorsement that shapes consumer perception of efficacy even before the product is used.

Where V-Beauty Sits – and Where It Does Not

Vietnamese beauty brands are not absent from the brightening category. They are prominent within it. Brightening claims built around turmeric, rice water, and centella asiatica appear across the V-beauty product landscape, from Cocoon’s Hung Yen turmeric lines to the rice water formulations documented across multiple Vietnamese brands.

The ingredient foundation is genuinely strong. Turmeric has a documented history of use in Vietnamese skincare and traditional medicine. Its active compound, curcumin, has been studied for anti-inflammatory and antioxidant properties that have indirect relevance to skin tone and pigmentation. Rice water contains ferulic acid, inositol, and vitamins that have moisturizing and mild brightening effects. Centella asiatica – rau má in Vietnamese – has the strongest clinical evidence base of any ingredient commonly used in V-beauty, with documented effects on wound healing, collagen synthesis, and skin barrier function.

The honest assessment, however, is that the claims Vietnamese brands make about these ingredients regularly outpace the evidence available to substantiate them. Turmeric’s brightening efficacy in cosmetic formulations – as opposed to pharmaceutical concentrations – is poorly documented in peer-reviewed literature. Rice water’s brightening effects are real but modest and well below the efficacy threshold that premium consumers in China, Korea, or Western markets now expect from a product at a premium price point. Centella’s benefits are primarily soothing and barrier-focused rather than brightening.

This is not a uniquely Vietnamese problem. As this site noted in its guide to turmeric in skincare: “The gap between the marketing and the evidence is worth closing.” That gap is widest precisely in the category – brightening – where premium consumer demand is currently concentrated.

The practical consequence is a positioning mismatch. V-beauty brands with genuine ingredient heritage and cultural provenance are structurally positioned for the premium functional brightening segment. Their actual product claims and clinical documentation position them in the lower end of that segment, competing on story rather than on evidence.

The Competitive Landscape They Are Entering

The premium brightening segment that V-beauty is positioned to enter is also the segment that the best-resourced brands in the world are currently fighting over.

L’Oréal’s La Roche-Posay, powered by Melasyl, has made anti-pigmentation its primary growth driver globally. SkinCeuticals crossed the billion-euro threshold in 2025, partly based on its Discoloration Defense serum. Eucerin’s Thiamidol brightening technology – a proprietary molecule with published clinical data on tyrosinase inhibition – anchored the Derma division’s fifth consecutive year of double-digit growth at Beiersdorf.

These are not heritage brands competing on ingredient storytelling. They are dermatological brands competing on clinical evidence, and they are winning the premium brightening consumer in every market where that consumer is making efficacy-first purchasing decisions.

K-beauty is playing in the same space with a different model: ingredient transparency, accessible premium pricing, and the credibility that comes from consumer-driven ingredient literacy communities on Xiaohongshu, TikTok, and Reddit. When Beauty of Joseon releases a rice-based serum with a disclosed niacinamide concentration and a published formulation rationale, it is competing on the same axis as La Roche-Posay – evidence. It is also maintaining the cultural accessibility that makes K-beauty different from clinical skincare.

V-beauty’s competitive position in this environment depends on its ability to close the gap between ingredient heritage and clinical substantiation. The heritage is real and defensible. The clinical investment required to convert that heritage into evidence-based premium positioning has not yet been made at scale by any Vietnamese brand.

The Timing Problem

The brightening market split creates a window for V-beauty – and simultaneously a deadline.

The window exists because the premium functional brightening segment is growing faster than mass-market tone-up, and the natural ingredient positioning that Vietnamese brands occupy is culturally compelling to a consumer base that is increasingly skeptical of synthetic actives. A Vietnamese brand that can credibly substantiate its brightening claims with clinical data would be entering a segment where the combination of efficacy and authentic ingredient provenance is genuinely differentiated.

The deadline exists because that window is not permanent. As Melasyl, Thiamidol, and proprietary K-beauty formulations consolidate their positions in premium brightening globally, the evidence bar rises and the space for heritage-only positioning narrows. The consumer who is currently open to a turmeric brightening serum from Vietnam is the same consumer who will, in three to five years, expect that turmeric serum to have the same kind of clinical data. They compared it against the niacinamide serum.

Skin-brightening creams already hold the dominant share of Vietnam’s skincare market by category, driven by cultural beauty standards that favor luminous, even-toned skin. The domestic consumer demand is there. The ingredient foundation is there. What remains is the clinical investment – and whether Vietnamese brands will make it before the premium brightening segment becomes a competition they can no longer enter on their terms.

The timing is good. The execution is not yet there.

Sources: Premium Beauty News, “The Evolution and Repositioning of Brightening Across Global Markets,” May 2025; Qingyan Intelligence (青眼情报), China High-End Beauty Market & Consumer Trends Report 2025; Dewsia, Turmeric in Skincare: What It Actually Does; Dewsia, Centella Asiatica in Vietnamese Skincare; L’Oréal 2025 Annual Results (official press release); Beiersdorf AG 2025 Annual Results.